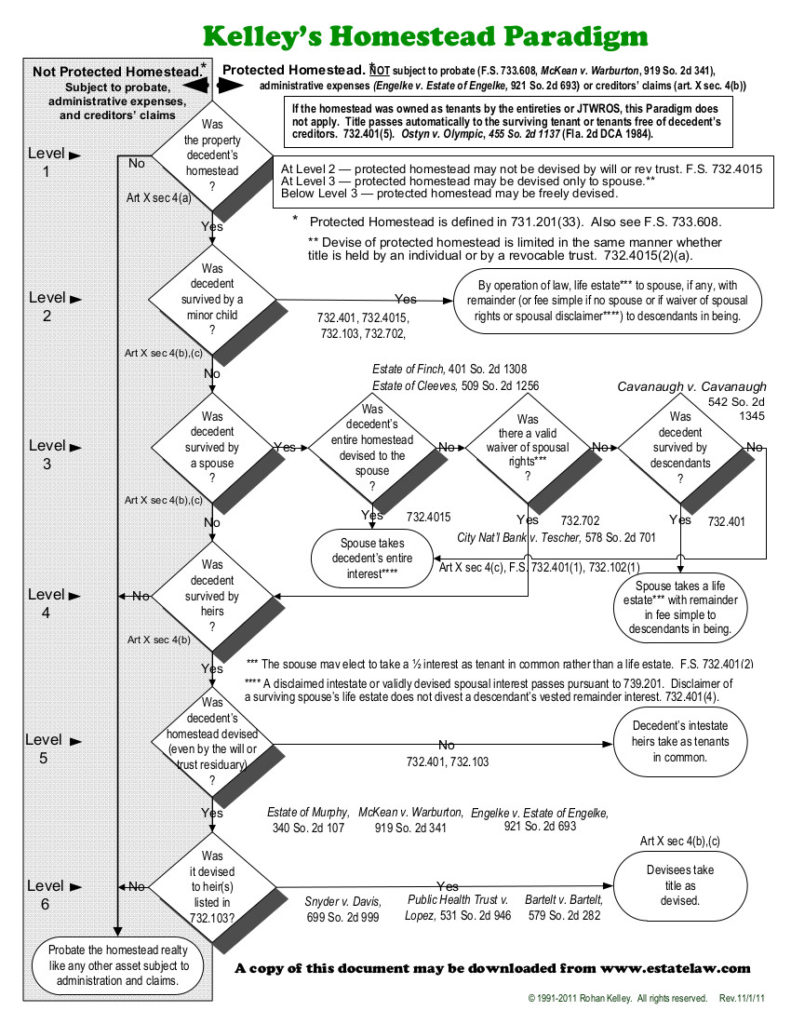

Kelley’s Homestead Paradigm

Kelley’s Homestead Paradigm is a decision-tree flowchart created by Florida attorney Rohan Kelley and first published in the March 1991 issue of the Florida Bar Journal. The paradigm maps every possible outcome for a Florida homestead property when its owner dies. It does this by walking through a series of yes-or-no questions that determine who inherits the property, whether the owner could have devised it by will, and whether the constitutional protection from creditors survives the transfer.

The paradigm matters for asset protection because Article X, Section 4(b) of the Florida Constitution provides that homestead exemptions “shall inure to the surviving spouse or heirs of the owner.” That language means the creditor shield does not automatically expire at death. Whether it actually carries forward, however, depends on the specific descent path the property follows. The paradigm identifies exactly where protection continues and where it falls away.

How the Paradigm Works

The paradigm contains a preliminary threshold question followed by six levels of analysis. Each level corresponds to a specific constitutional or statutory provision.

Preliminary Question: Is the Property Protected Homestead?

Before the paradigm’s branching logic begins, the threshold inquiry asks whether the property qualified as protected homestead at the moment of the owner’s death. This requires that all constitutional elements were satisfied: the property was owned by a natural person, the owner (or the owner’s family) occupied the property as a permanent residence, and the property fell within the size and contiguity limits of Article X, Section 4(a).

If the property was not protected homestead at death, the analysis stops. The property enters the probate estate as a general asset, available to pay the decedent’s debts. This can happen when the owner had abandoned the property, when the property was titled in an entity that cannot hold homestead (such as an LLC), or when the property exceeded the acreage limits without qualifying for the contiguity exception.

Assuming the property passes this threshold, the paradigm moves to the decision levels.

Speak With a Florida Asset Protection Attorney

Jon Alper and Gideon Alper have designed and implemented asset protection structures for clients since 1991. Consultations are confidential and conducted by phone or Zoom.

Book a Consultation

Level 1: Was the Property Owned by the Decedent?

The first formal question asks whether the decedent held an ownership interest in the property. If the decedent had no legal or equitable ownership interest at death, the property cannot be the decedent’s homestead and the analysis ends. The property falls into the gray column.

This level catches situations where the decedent had previously transferred title. A person who deeded the property to a child, for example, and then continued living there as a guest has no ownership interest to protect. It also addresses properties held in trusts. A revocable living trust preserves homestead status because the settlor retains the equitable interest and the power to revoke. An irrevocable trust raises more complicated questions about whether the beneficiary’s interest constitutes “ownership” for homestead purposes.

Level 2: Was the Decedent Survived by a Minor Child?

This is the most restrictive level in the paradigm. Article X, Section 4(c) of the Florida Constitution provides that homestead “shall not be subject to devise if the owner is survived by spouse or minor child.” When any minor child survives the owner, the homestead cannot be devised to anyone, by any instrument, under any circumstances. A will that purports to leave the homestead to the spouse, to an adult child, to a trust, or to any other person is void as to the homestead when a minor child exists.

The constitutional prohibition reflects a policy judgment that minor children must be provided for and cannot be left homeless by a parent’s testamentary decision.

Spouse and minor children survive. The homestead descends by operation of law under Section 732.401 of the Florida Probate Code. The surviving spouse receives a life estate, and all of the decedent’s descendants who are alive at the time of death receive a vested remainder interest, per stirpes. The spouse has the right to live in the home for life. The descendants hold a present ownership interest that takes effect when the life estate terminates.

The surviving spouse may elect, within six months of death, to take an undivided one-half interest as a tenant in common instead of the life estate. This election must be filed in the official records of the county where the property is located. The tenant-in-common election under Section 732.401(2) gives the spouse a present ownership stake rather than a mere right of occupancy. The remaining one-half vests in the descendants per stirpes.

The practical difference matters. A life estate cannot be partitioned. If the spouse and the descendants disagree about whether to sell, the property stays locked in the life estate until the spouse dies or voluntarily relinquishes the interest. A tenant-in-common interest can be partitioned. The spouse who elects the TIC option may petition the court to force a sale and receive half of the proceeds.

Minor children but no spouse. The homestead passes directly to the descendants in equal shares. Because minors cannot legally manage real property, a court-appointed guardianship of the property will be required until the youngest child reaches majority.

In both scenarios, creditor protection continues. The property passes outside probate and is not available to satisfy the decedent’s debts.

Level 3: Is There a Surviving Spouse?

If there are no minor children, the paradigm asks whether the decedent was survived by a spouse. The answer determines how much freedom the owner had to devise the homestead.

Spouse survives, no minor children. The constitutional restriction on devise still applies, but it loosens. The homestead may be devised, but only to the surviving spouse in fee simple. Nothing less than the decedent’s entire interest will suffice. The Florida Supreme Court held in In re Estate of Finch (1981) that a devise of a life estate to the spouse, a devise to the spouse and another person jointly, or a devise that bypasses the spouse entirely is constitutionally prohibited when a spouse survives.

If the decedent’s will makes a valid devise to the spouse in fee simple, the spouse takes the property outright. Creditor protection transfers with it.

If the will attempts an invalid devise (anything other than fee simple to the spouse), the devise is void and the property passes by intestate succession. When there are also surviving descendants, the spouse takes a life estate (or may elect the TIC option) and the descendants take the vested remainder. When there are no descendants, the spouse inherits the property in fee simple under Section 732.102.

Spousal waiver. The paradigm accounts for the possibility that the spouse waived homestead devise rights before the owner’s death. Under Sections 732.702 and 732.7025, a spouse may waive these rights through a prenuptial agreement, a postnuptial agreement, or by joining in a deed with specific waiver language. If the waiver is valid and there are no minor children, the constitutional restriction falls away and the homestead may be devised freely.

Importantly, Section 732.7025 provides that a waiver of homestead devise rights does not waive the creditor protection. The homestead remains shielded from forced sale even though the spouse has given up the right to inherit it.

No spouse, no minor children. The constitutional restriction on devise does not apply. The analysis moves to Level 4.

Level 4: Does the Decedent Have Any Heirs?

When neither a spouse nor a minor child survives, the paradigm asks whether the decedent has any heirs at law as defined by Section 732.103 of the Florida intestacy statutes. This is where a second type of creditor risk enters the analysis.

If the decedent has no heirs at law, the homestead loses its protected status. The property becomes a probate asset, subject to creditor claims and the expenses of estate administration. Under Section 732.107, property with no taker escheats to the state.

If heirs exist, the protection remains intact and the analysis continues.

Level 5: Was the Homestead Devised?

This level asks whether the decedent left a will or trust that devised the homestead to someone. If the homestead was not devised, it descends by intestate succession to the heirs defined in Section 732.103. The heirs take the property as tenants in common, and the creditor protection passes with it. This is the simplest outcome at this stage of the paradigm.

If the homestead was devised, the analysis moves to the final question.

Level 6: Was the Property Devised to an Heir at Law?

The final decision point determines whether the creditor protection survives a devise to a specific person. The question is whether the devisee qualifies as an heir at law under the intestacy statutes.

Devise to an heir at law. If the devisee is a person listed in Section 732.103, the creditor protection continues. The devisee takes the property free of the decedent’s creditor claims. This is true even if other heirs exist who were not named in the will. The will controls which heir receives the property; the paradigm only requires that the recipient fall within the statutory class.

Devise to a non-heir. If the devisee is someone outside the class of intestate heirs, the creditor protection is lost. The property becomes a general asset of the probate estate, available to satisfy the decedent’s debts and the costs of administration. The First District Court of Appeal addressed this scenario in Webb v. Blue (2018), where the decedent left his homestead to a friend. Because the friend was not an heir at law, the court held that the property entered the probate estate.

This is the paradigm’s final fork. The property either retains its protection and passes to the named heir, or it loses protection and becomes available to creditors.

The Blended Family Problem

The paradigm’s structure reveals why homestead planning is especially difficult for blended families. Consider a homeowner who is married, has adult children from a prior marriage, and wants the children to inherit the home rather than the current spouse. The Constitution prohibits any devise other than fee simple to the spouse when a spouse survives. If the owner dies without addressing this, the spouse gets a life estate and the children get the vested remainder, creating a shared ownership structure that neither party may want.

The spousal waiver is the primary planning tool here. If the spouse executes a valid waiver of homestead devise rights, the owner can devise the property to the adult children. The children qualify as heirs at law, so the creditor protection survives under Level 6 of the paradigm.

Without the waiver, the spouse’s life estate vests automatically at death. A post-death disclaimer by the spouse cannot cure an invalid devise. The vested remainder that passes to descendants at the moment of death cannot be stripped away by a later spousal action. This principle was established in In re Estate of Ryerson (Fla. 15th Cir. 1993), where the court held that a spousal disclaimer could not divest the adult children of their vested remainder interest.

Tenants by the Entirety as a Planning Override

One way to bypass the paradigm’s restrictions entirely is to title the homestead as tenants by the entirety between spouses. When property is held as tenants by the entirety, the surviving spouse takes full ownership by operation of law at the first spouse’s death. The property does not pass through the devise analysis at all because the survivorship feature of entireties ownership is an inter vivos transfer, not a testamentary one.

This approach works when the goal is to leave the property outright to the surviving spouse. It does not work when the goal is to leave the property to someone other than the spouse, because the survivorship feature cannot be overridden by a will.

Sale Proceeds After Death

One question the paradigm does not directly address but that practitioners frequently encounter is what happens when the heirs sell the homestead after the owner’s death. The Second District Court of Appeal answered this in In re Estate of Hamel (2002), holding that because the heirs’ homestead rights vested at the moment of death, the sale proceeds from a subsequent sale remained protected from the decedent’s creditors.

This holding confirms that the creditor protection identified in Levels 2 through 6 of the paradigm is not limited to continued occupancy by the heirs. The protection attaches to the property interest itself and follows it into liquid form if the heirs choose to sell.

Planning With the Paradigm

The paradigm is more than a probate tool. It identifies the decisions that must be made during the homestead owner’s lifetime to control which path the property follows after death.

An owner who wants the spouse to inherit outright should either devise the homestead to the spouse in fee simple (permissible when there are no minor children) or title the property as tenants by the entirety. An owner who wants children from a prior marriage to inherit should obtain a valid spousal waiver before death.

An owner with no spouse and no minor children who wants to preserve the creditor protection for the devisee should ensure the devisee is an heir at law under Section 732.103. An owner who wants to leave the property to a friend, charity, or other non-heir should understand that the creditor protection will be lost when the property enters probate.

Each of these decisions maps directly to a level of the paradigm. The flowchart does not create the rules. It organizes them in a way that makes the consequences visible before they become irreversible.