Offshore Trusts

An offshore trust is a type of trust used to move assets to a foreign country where courts do not recognize U.S. judgments. A creditor cannot force a foreign trustee to hand over assets, produce records, or comply with a domestic court order. The only path for the creditor is to hire a lawyer in the offshore jurisdiction, post a bond, and relitigate the claim under rules that heavily favor the settlor.

In the Cook Islands, where most U.S. offshore trusts are established, no creditor has ever recovered assets through local proceedings. An offshore trust is the strongest asset protection structure available for people with substantial non-exempt wealth who face or anticipate personal liability.

Speak With a Cook Islands Trust Attorney

Jon and Gideon Alper specialize in creating Cook Islands trusts for clients nationwide. Consultations are free and confidential, by phone or Zoom, and usually available within one business day. You’ll speak directly with the attorney.

See Pricing & Book a Consultation

How Do Offshore Trusts Work?

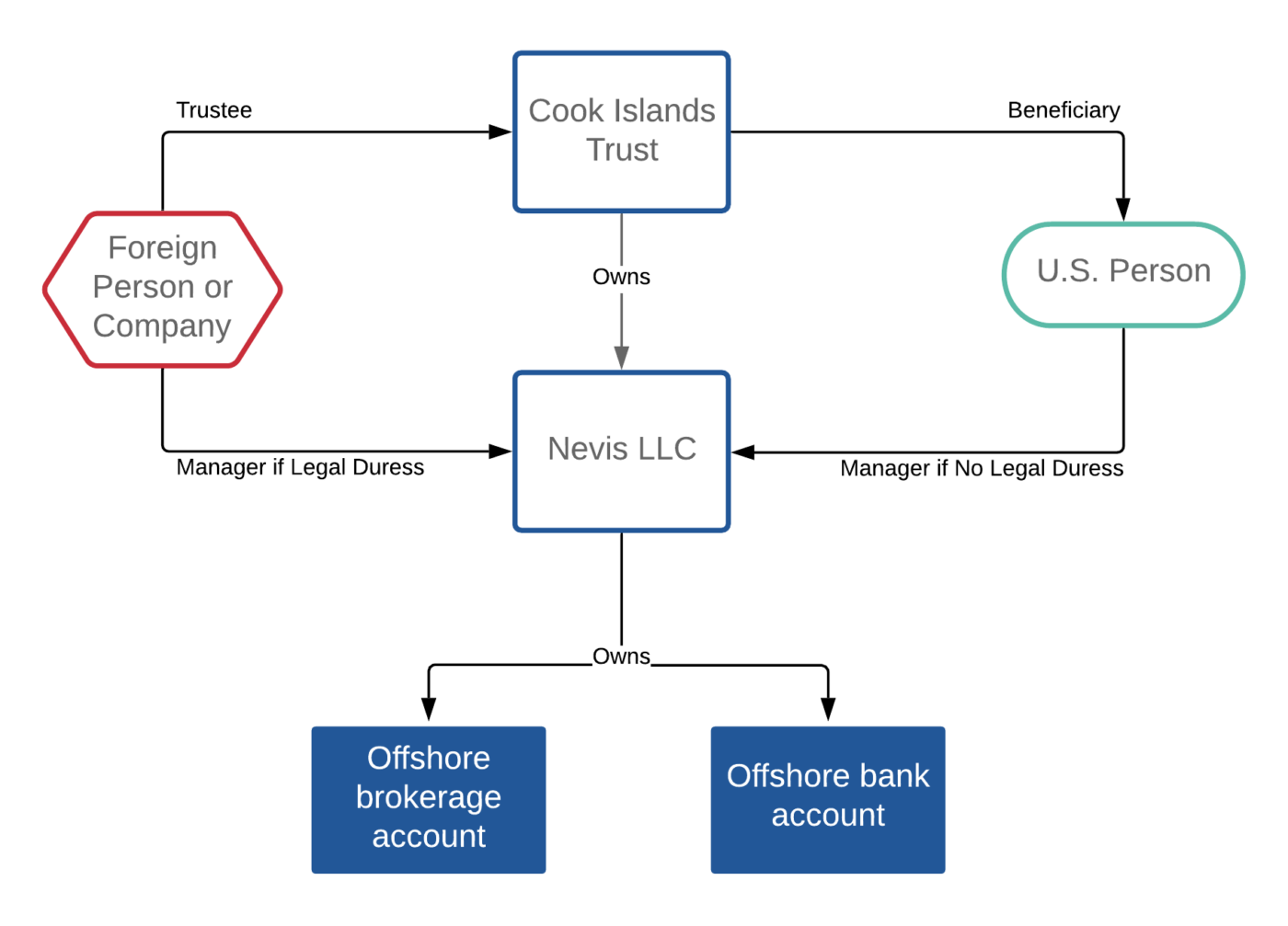

An offshore trust is governed by the law of the country where it is established. The trustmaker signs a trust deed naming a licensed foreign trust company as trustee and transfers assets into the trust. Assets can move directly into the trust or into a holding entity, typically a Nevis LLC or Cook Islands LLC, owned by the trust. Once funded, the trustee holds legal title and manages the assets under the terms of the trust deed.

The trustmaker is usually also the primary beneficiary. The trust deed gives the trustee discretion over distributions, meaning the trustee decides whether and when to release funds. If the trustmaker could withdraw assets at will, a court could simply order the withdrawal and redirect the funds to a creditor. Because the trustee controls distributions, that order has nothing to reach.

The trustmaker can request distributions, and in ordinary circumstances the trustee honors those requests. But the trustee has no legal obligation to comply. When a lawsuit or creditor threat arises, the trustee’s ability to say “no” is the mechanism that keeps assets out of reach.

The trustmaker, trustee, and protector each hold defined powers, and the trust’s duress clause directs the trustee to refuse any instruction that a creditor forces the trustmaker to give.

Typical Structure

Most offshore trust plans pair a Cook Islands trust with a Nevis LLC or Cook Islands LLC. The trust owns 100% of the LLC. The trustmaker serves as manager of the LLC during ordinary times, keeping day-to-day control over investments and bank accounts held within the LLC.

When a creditor threat arises, the trustee removes the trustmaker as LLC manager and takes direct control, placing the assets beyond any U.S. court order. Once the threat passes, the trustmaker is restored as manager. The trust deed, LLC operating agreement, and trustee protocols govern exactly how this transition works.

Removing the trustmaker as LLC manager does not require the trustmaker’s consent or a court order. The trustee acts unilaterally under the trust deed.

Advantages of Offshore Trusts

Offshore trusts provide four primary advantages: creditor protection, financial privacy, estate planning, and jurisdictional diversification.

1. Creditor Protection

An offshore trust puts assets beyond a creditor’s practical reach by placing them under the control of a foreign trustee who does not answer to U.S. courts. The Cook Islands imposes a two-year statute of limitations on fraudulent transfer claims, requires proof beyond a reasonable doubt, and refuses to enforce foreign judgments.

Even when a creditor declines to pursue offshore litigation, the trust still makes settlement more likely. A creditor facing years of enforcement effort against a foreign trustee who will not comply with U.S. orders is more likely to accept a reduced settlement rather than spending more on enforcement than the claim is worth.

2. Financial Privacy

Offshore trusts are not listed in any public database. The trust deed is a private document executed in a foreign country. No U.S. public filing reveals who owns a Cook Islands trust or what assets it holds. The IRS knows about the trust through required tax filings, but creditors, business competitors, and the general public do not.

3. Estate Planning

An offshore trust directs how assets pass to beneficiaries at death without probate, and the creditor protection continues for the next generation. The trust’s ongoing management, succession, and eventual termination determine how long the protection lasts and how wealth transfers across generations.

4. Jurisdictional Diversification

A person whose entire net worth sits within the U.S. legal system is fully exposed to its courts and political environment. An offshore trust moves a portion of those assets to a country whose laws favor the asset owner. Political and systemic risks that drive people toward offshore planning include capital controls, bank failures affecting uninsured deposits, dollar devaluation, and concentration of financial exposure within a single legal system.

Disadvantages of Offshore Trusts

The main disadvantages of an offshore trust are bankruptcy vulnerability, loss of direct asset control, and ongoing compliance costs.

1. Bankruptcy Vulnerability

Offshore trusts are weakest in bankruptcy. Federal bankruptcy trustees have worldwide jurisdiction over a debtor’s assets. The Bankruptcy Code requires the debtor, not the creditor, to bring assets to the trustee. Under § 548(e)(1), a bankruptcy trustee can claw back transfers to self-settled trusts made within ten years of filing. In In re Huber (2013), a bankruptcy court reached assets in a Cook Islands trust, demonstrating that bankruptcy is the one context where offshore protection can fail. No one with an offshore trust would voluntarily file for bankruptcy, but involuntary petitions are a real risk.

2. Losing Direct Control of Your Assets

The trustmaker of an offshore trust must give up direct access to assets transferred into it. This is by design. When a court orders a trustmaker to repatriate assets, the defense to a possible contempt order is that the trustmaker genuinely cannot comply. That defense only works if the loss of control is real. The contempt and repatriation risk is the most frequently litigated aspect of offshore trust enforcement.

3. Certain Assets Are Hard to Protect

Poorly timed asset transfers create fraudulent transfer exposure. U.S. real estate held through a trust remains within U.S. court jurisdiction regardless of the trust’s location. IRS reporting penalties for missed filings can exceed the cost of the trust itself. Each of these offshore trust risks narrows the pool of people for whom the structure makes economic sense.

Setup Process

Setting up an offshore trust involves five steps:

- Select the jurisdiction. The Cook Islands offers the strongest combination of trustee regulation, favorable statutes, and litigation track record. Nevis is the primary alternative for trustmakers prioritizing cost.

- Choose a licensed trustee company. Licensed Cook Islands and Nevis trustees are regulated by their local governments and subject to capital and insurance requirements. The attorney generally has established relationships with several trustees and can match the trustmaker with the company that best fits the asset profile.

- Complete due diligence. Trust companies run background checks on the trustmaker and beneficiaries, verifying identity, source of funds, and current legal situation. Pending lawsuits must be disclosed. Most trustmakers clear the vetting without difficulty, though the trustee may require the trust deed to address any existing creditor under a Jones clause.

- Draft the trust deed and entity documents. The attorney drafts the offshore trust agreement, the operating agreement for any LLC in the structure, and any domestic entity paperwork.

- Fund the trust. Assets move to the offshore LLC or directly to the trustee. Liquid assets transfer most cleanly. U.S. real estate requires a different approach because the property remains within U.S. court jurisdiction.

Cook Islands trusts can be established after a lawsuit has been filed. The trust deed includes a Jones clause that authorizes the trustee to pay the existing creditor under defined conditions, reducing fraudulent transfer exposure and providing a contempt defense. Post-claim planning carries higher contempt risk and weaker negotiating leverage than planning done before litigation exists.

Planning typically takes four to eight weeks from engagement to a funded trust.

Requirements of Offshore Trusts

Here are the requirements for an offshore trusts to be protected from U.S. creditors:

- The trust must be irrevocable. A revocable trust offers no creditor protection because the trustmaker retains the power to demand the assets back, which a court can compel.

- The trustmaker cannot act as trustee. A trustmaker who holds trustee power can be ordered to act on the trust’s behalf.

- The trustee must be a licensed foreign trust company, not an individual and not a U.S. entity. Licensed trust companies in the Cook Islands and Nevis are regulated, bonded, and experienced in asset protection.

- The trustee must have discretion to withhold distributions. The anti-duress clause directs the trustee to refuse distributions when the trustmaker is under legal duress from a U.S. creditor.

- The trust protector, if any, must be located outside the United States. A U.S.-based protector is subject to U.S. court jurisdiction and can be compelled to remove or replace the trustee.

- The choice-of-law clause must name the offshore jurisdiction. The trust deed must state that the laws of the Cook Islands or Nevis govern the trust’s validity and administration.

- Assets must move offshore or into an offshore entity controlled by the trustee. Assets physically located in the United States remain subject to U.S. court jurisdiction regardless of who holds title.

A licensed offshore trustee holds no beneficial interest in the trust, and its independence from the trustmaker is what lets the structure withstand a U.S. court order.

See What a Cook Islands Trust Costs

Our legal fee for a Cook Islands trust is $15,000. Consultations are free and confidential, by phone or Zoom, and you’ll speak directly with the attorney.

See Pricing & Book a Consultation

How Much Does an Offshore Trust Cost?

A Cook Islands offshore trust costs about $21,000 to establish and about $5,000 per year in trustee fees thereafter. Setup fees cover drafting the trust deed, coordinating with the foreign trustee, forming any related entities, and completing the initial regulatory vetting.

Annual maintenance covers trustee administration, U.S. tax compliance (Forms 3520, 3520-A, FBAR, and Form 8938), and banking fees. The CPA handles all ongoing tax filings. The attorney structures the trust but does not manage annual compliance.

These costs make offshore trusts impractical for individuals with modest assets or low litigation risk. The minimum net worth at which the economics work is roughly $1 million in total assets or $500,000 in liquid non-exempt wealth.

Are Offshore Trusts Legal?

Offshore trusts are legal. No U.S. law prohibits a citizen or resident from creating a trust in a foreign country, transferring assets to a foreign trustee, or maintaining foreign bank accounts. The legal boundary is disclosure—not the structure itself.

The IRS imposes reporting obligations on U.S. persons who create or fund foreign trusts, and the penalties for noncompliance are among the harshest in the tax code. A properly structured and fully reported offshore trust is entirely lawful. An unreported one is not.

How Are Offshore Trusts Taxed?

An offshore trust created by a U.S. person is treated as a grantor trust for tax purposes. The IRS looks through the trust entirely—the trust pays no taxes. All income, gains, losses, and deductions flow through to the trustmaker’s personal return, exactly as if the assets were still held directly. An offshore trust does not reduce, defer, or eliminate any U.S. tax obligation.

The IRS reporting requirements include Forms 3520 and 3520-A annually, FBAR filings for foreign accounts exceeding $10,000 in aggregate value, and Form 8938 under FATCA. Missing a filing can trigger a $10,000 penalty per form annually. Continued nonfiling escalates to 5% of the trust’s total assets. A CPA handles all offshore trust tax filing and reporting. This is accounting work, not legal work.

Which Countries Are Best for Offshore Trusts?

The Cook Islands is the strongest offshore trust jurisdiction. Its trust law has been tested in U.S. litigation more than any other offshore country, and no creditor has recovered assets through Cook Islands proceedings. The Cook Islands imposes a two-year statute of limitations on fraudulent transfer claims, requires proof beyond a reasonable doubt, and does not recognize foreign judgments.

Nevis offers a viable alternative at a lower cost. Nevis law requires creditors to post a bond (typically around $100,000) before initiating litigation, does not recognize foreign judgments, and imposes a two-year limitations period. The comparison between Cook Islands and Nevis trusts turns on whether the Cook Islands’ deeper litigation track record justifies its higher cost.

The best offshore trust countries differ in their burden-of-proof standards, limitation periods, and enforcement histories. For most U.S. residents seeking creditor protection, the Cook Islands remains the first choice.

Who Should Consider an Offshore Trust?

Offshore trusts are appropriate for individuals whose litigation exposure and asset level justify the cost. The people who benefit most hold $500,000 or more in liquid wealth, face above-average creditor risk from their profession or business activities, and have exhausted the domestic planning alternatives available in their state.

Private placement life insurance is marketed to the same audience: PPLI shelters investment gains from income tax, while an offshore trust blocks creditor collection, and the two structures are sometimes combined.

Physicians, business owners, contractors, real estate investors, and other high-risk professionals each face distinct liability patterns that shape how the trust is structured and funded. Whether planning is proactive, triggered by a filed lawsuit, or timed around a liquidity event determines which trust provisions matter most.

In divorce, an offshore trust can limit a spouse’s ability to enforce property division and support orders against trust assets, though family courts have broader equitable powers than most creditors. For cryptocurrency, an offshore trust addresses both protection and custody, since digital assets can be moved to the trustee’s control more easily than most other asset types. Real estate presents the opposite challenge: U.S. property stays within U.S. court jurisdiction regardless of who holds title. Funding considerations differ across asset types including stock portfolios, business interests, and intellectual property.

Offshore Trust vs. Domestic Trust

Several U.S. states, including Nevada, South Dakota, Alaska, and Delaware, allow self-settled asset protection trusts that, on paper, compete with offshore trusts. Domestic asset protection trusts cost less, carry no foreign reporting obligations, and use trustees located in the United States.

However, domestic asset protection trusts can only reliably protect people who live in a state that has enacted a DAPT statute. A creditor can sue in the debtor’s home state, and if that state has no DAPT law, the court will likely apply local law rather than the DAPT state’s law, rendering the trust useless. For residents of non-DAPT states, which is the majority of the country, a domestic trust is not a reliable strategy.

Even for DAPT-state residents, domestic trusts have two additional vulnerabilities. Federal bankruptcy jurisdiction under § 548(e)(1) imposes a ten-year lookback, and a U.S. bankruptcy trustee can compel a domestic trustee to comply, while a Cook Islands trustee is beyond reach. Most DAPT statutes also have limited or no appellate case law confirming they work as intended, while Cook Islands trust law has been tested in U.S. litigation for more than 30 years.

An offshore trust avoids these problems because the trustee operates in a country that refuses to recognize U.S. court orders. The offshore trust vs. domestic trust distinction is structural: a U.S. judge can compel a domestic trustee but cannot compel an offshore one. State-by-state comparisons of offshore trusts against domestic trusts in Nevada, Wyoming, and other DAPT states show these vulnerabilities apply to all domestic trusts.

Bridge Trust Alternative

A bridge trust is a domestic trust that can migrate to an offshore jurisdiction when triggered by specific events, typically the filing of a lawsuit or the entry of a judgment. For individuals who want offshore protection but are not ready to commit to a full offshore structure, a bridge trust reduces upfront costs and avoids foreign trust reporting while no offshore structure is in place.

The tradeoff is that the protection is not yet activated. If a creditor moves faster than the migration can execute, the assets may still be within reach. A bridge trust is a middle-ground option, not a substitute for an offshore trust that is already funded and in place.

Hungarian Trusts

Hungary enacted trust legislation in 2014 that allows foreign individuals, including U.S. citizens, to create trusts under Hungarian law. A creditor must prove fraudulent transfer beyond a reasonable doubt and must bring the action in Hungary. The Hungarian trust has attracted interest from European individuals and some U.S. planners seeking an EU-based alternative.

The Hungarian trust offers advantages in EU regulatory recognition and access to tax treaties, but it lacks the decades-long litigation track record that the Cook Islands and Nevis have built. For U.S. residents whose primary goal is creditor protection, the Cook Islands remains the stronger choice.

Offshore Trust Financial Accounts

An offshore trust holds assets through foreign bank or brokerage accounts at institutions without U.S. branches, placing the accounts beyond the subpoena power of U.S. courts. The trustee—not the trustmaker—is the account holder and signatory. The trustmaker can request distributions, and in ordinary times the trustee processes them routinely, but the trustmaker has no independent account access.

Opening foreign bank accounts as an individual U.S. citizen has become increasingly difficult. Most reputable foreign banks no longer accept individual U.S. applicants because of FATCA compliance costs. The offshore trust or LLC structure provides the workaround: the foreign entity opens the account, and the trustee maintains the banking relationship. Offshore bank accounts held within the trust structure require careful selection based on the institution’s willingness to work with Cook Islands or Nevis entities and its U.S. reporting infrastructure.

Alper Law has structured offshore and domestic asset protection plans since 1991. Schedule a consultation or call (407) 444-0404.