Cook Islands Trusts

A Cook Islands trust is a special type of trust that can protect assets from creditors by moving them to a foreign country that does not recognize U.S. judgments. With a Cook Islands trust, a foreign trustee company holds legal title to the assets for the benefit of the person who sets up the trust.

No creditor has successfully recovered assets from a properly established Cook Islands trust in more than three decades of contested litigation.

How Does a Cook Islands Trust Work?

A U.S. court judgment has no legal effect in the Cook Islands. A creditor cannot enforce its judgment against the trustee company located there. The creditor must instead file a new proceeding in the Cook Islands, hire Cook Islands counsel, and relitigate the claim from scratch under Cook Islands law.

In our experience, most creditors settle their claim when faced with the prospect of having to collect against assets located offshore in a Cook Islands trust.

Roles

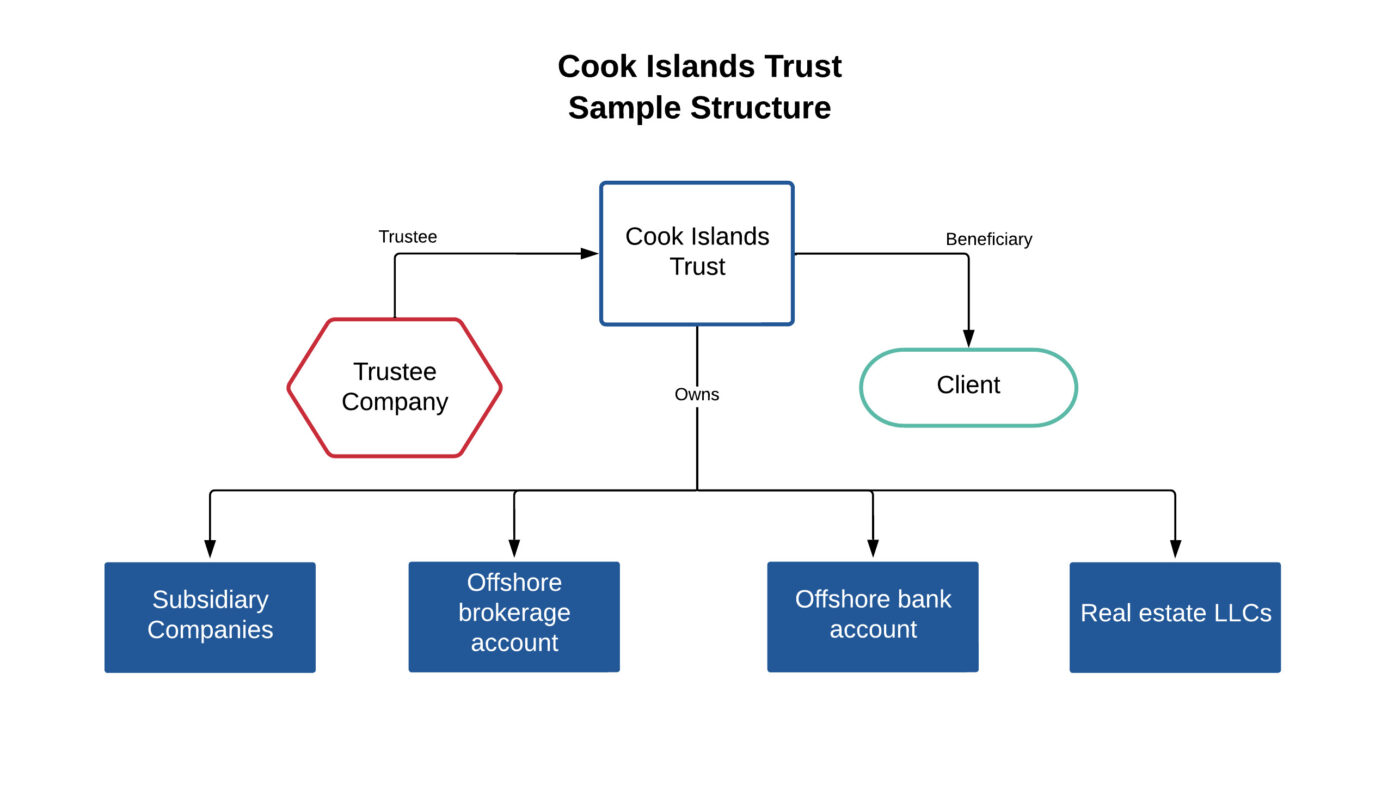

A Cook Islands trust has four parties: the settlor, the trustee, the beneficiary, and the trust protector.

The settlor creates the trust and transfers assets into it.

The trustee is a licensed Cook Islands trust company that holds legal title and administers the trust under Cook Islands law. Every licensed trustee is insured and bonded through the Financial Supervisory Commission.

The beneficiary is the person entitled to receive distributions. The trust settlor is almost always the primary beneficiary.

A trust protector has the authority to remove and replace the trustee if needed. Appointing a trust protector is optional, and most Cook Islands trust setups do not need one.

A trust deed defines each party’s role and the rules governing trustee conduct.

Speak With an Offshore Trust Attorney

Jon and Gideon Alper design offshore trusts for clients nationwide. Consultations are free and confidential, by phone or Zoom, and usually available within one business day.

Request a Free Consultation

Advantages

Cook Islands law creates four barriers that make creditor collection impractical:

First, the creditor must prove fraudulent transfer beyond a reasonable doubt, the criminal standard of proof rather than the civil preponderance standard used in U.S. courts.

Second, the creditor must post a bond of at least $100,000 with the Cook Islands court before filing. If the creditor loses, the bond is forfeited to cover the trust’s legal costs.

Third, the statute of limitations is short. A creditor must file within two years after funding the trust or one year after their cause of action arose, whichever expires sooner. Once the deadline passes, the Cook Islands courts will not hear the claim. Each transfer starts its own clock.

Fourth, the trust deed contains a duress clause that prevents the trustee from following the settlor’s instructions when those instructions are made under court pressure. If a U.S. court orders the settlor to repatriate trust assets, the duress clause activates, and the trustee refuses. The settlor can show the court that they asked the trustee to comply and were refused, creating what courts have called an “impossibility” defense.

Disadvantages

There are three main disadvantages of a Cook Islands trust: reduced control over trust assets, ongoing U.S. tax compliance, and exposure to contempt proceedings in U.S. courts.

Reduced Control

Cook Islands trusts require the settlor to give up direct control over assets and to accept that any dispute with the trustee must be resolved under Cook Islands law, not U.S. law. Cook Islands trustee companies are licensed and regulated by the Cook Islands Financial Supervisory Commission, and no trustee has ever misappropriated a settlor’s assets. The legal recourse for any dispute runs through Cook Islands courts, not U.S. courts.

Ongoing Tax Compliance

A Cook Islands trust provides no tax benefit. The IRS treats a Cook Islands trust as a grantor trust. All income, gains, and deductions flow through to the settlor’s personal return, and the settlor pays the same taxes as if the assets were held directly.

U.S. persons with a Cook Islands trust must file Forms 3520 and 3520-A annually, report foreign financial accounts on the FBAR (FinCEN Form 114), and file Form 8938 when specified foreign financial assets exceed the applicable threshold. The CPA handles these filings, not the attorney. Penalties for non-compliance start at $10,000 per form per year. These compliance obligations are driven by U.S. law and apply each year regardless of whether the trust generates income.

A Cook Islands trust must be disclosed on tax returns, in discovery proceedings, and in response to lawful court inquiries. Attempting to conceal a trust is illegal and counterproductive.

Contempt Exposure

Even with a properly structured trust, a U.S. court can hold the settlor in civil contempt for refusing a repatriation order. The order can stand even when the trustee independently declines to release the assets. The duress clause and impossibility defense mitigate contempt exposure but do not eliminate it.

Cook Islands trusts are strongest for liquid assets held in offshore accounts. Real estate sitting inside the U.S. is harder to protect because courts can directly control domestic real property through in rem proceedings, regardless of title.

Cost to Set Up a Cook Islands Trust

A Cook Islands trust costs $15,000 to $20,000 in legal fees to establish and $5,000 to $8,000 annually in trustee fees to maintain. The annual fee covers trustee administration, custodial fees at the offshore bank or brokerage, and ongoing coordination between the trustee and the settlor’s advisors.

U.S. tax preparation for the required foreign trust returns adds $2,000 to $3,000 per year. The settlor’s CPA handles these filings, not the attorney or trustee.

The cost structure varies based on asset complexity and the number of entities involved. Situations involving multiple LLCs, real estate, or business interests cost more than a single trust holding a brokerage account. Litigation-related expenses, such as trustee intervention when a creditor files a claim, are additional.

Cook Islands trusts are not cost-effective for everyone. The planning threshold is $1 million in total assets or $500,000 in liquid assets. Below that level, the setup and maintenance costs consume too large a share of the protected assets. People with lower asset levels can often achieve meaningful protection through domestic structures and state exemptions.

Who Needs a Cook Islands Trust?

Cook Islands trusts are built for people whose liability exposure and non-exempt assets are large enough to justify the cost and complexity. The typical candidate is a physician, business owner, real estate developer, or high-net-worth professional with at least $1 million in total assets or $500,000 in liquid assets.

People in professions with elevated litigation risk benefit most because the trust changes the creditor’s math before a lawsuit is filed. A creditor who knows the target’s liquid assets sit in a Cook Islands trust faces a collection process that will take years, cost six figures, and likely fail. Plaintiffs’ attorneys working on contingency often decline these cases for that reason.

Common Structure

Most Cook Islands trusts use an LLC holding structure. The trust owns an offshore LLC, and the LLC holds the bank and brokerage accounts where assets are kept. The settlor is appointed as the LLC’s initial manager, retaining day-to-day control over investments during normal circumstances.

When a legal threat arises, the trustee replaces the settlor as LLC manager and takes control of the assets. Removing the settlor as LLC manager does not require the settlor’s consent or a court order. The trustee acts unilaterally under the trust deed.

The LLC manager replacement is the moment most settlors find difficult to internalize during planning. Signing over manager authority to a Cook Islands trustee looks straightforward on paper. The hesitation arrives later, when the settlor sits with the prospect of losing day-to-day control during a credible threat. We typically address it during the planning conversation by walking through what the replacement actually triggers and what the settlor’s role looks like afterward. The replacement is not automatic on funding. It is reserved for the specific event of a credible legal threat.

How Do You Set Up a Cook Islands Trust?

Setting up a Cook Islands trust involves four steps:

- Select a licensed Cook Islands trust company as the trustee.

- Complete the KYC and AML background check that Cook Islands anti-money laundering laws require.

- Have the trust deed drafted by a U.S. attorney who structures the defensive provisions, identifies the parties, and coordinates with the trustee.

- Fund the trust by transferring assets to the offshore accounts.

The process takes three to eight weeks from engagement to funded trust. The timeline depends mainly on how quickly the settlor gathers documentation and completes the KYC process. The trustee’s KYC package typically includes a notarized passport or driver’s license copy, a bank reference letter, proof of address, documentation of the source of funds, and a sworn affidavit of solvency.

Cook Islands trusts can be established during active litigation. The trust deed includes a Jones clause that authorizes the trustee to pay the specific existing creditor under defined conditions, which mitigates fraudulent transfer exposure and provides a defense against contempt. Post-claim planning carries higher contempt risk and a weaker negotiating position than pre-claim planning, and it is not effective for protecting real estate. Liquid assets remain the strong case for post-claim formations.

What Can a Cook Islands Trust Protect Against?

Cook Islands trusts protect against civil judgments, including malpractice verdicts, business liability, personal injury claims, and contract disputes. A U.S. court can order the settlor to repatriate assets, but the trustee, operating under Cook Islands law, will decline to comply.

A Cook Islands trust can also protect against divorce. A U.S. family court can order equitable distribution of marital assets, but it cannot compel a Cook Islands trustee to comply. The trustee operates under Cook Islands law, not U.S. family court jurisdiction, and will not distribute trust assets to satisfy a foreign divorce judgment. Setting up a Cook Islands trust while married requires spousal consent and careful structuring to avoid creating grounds for a fraudulent transfer challenge.

Cook Islands trusts also provide insulation from political and systemic risks. Assets held offshore sit outside any single country’s banking and legal system, insulated from capital controls, bank failures affecting uninsured deposits above the $250,000 FDIC limit, and concentration risk.

Case Law

Cook Islands trusts have been tested in U.S. federal courts for more than 25 years. The results follow a pattern: U.S. courts can pressure the settlor, but they cannot reach the assets.

The strongest tool courts have used is civil contempt. In FTC v. Affordable Media, the court held both settlors in contempt for failing to return trust assets to the U.S. The Cook Islands trustee refused to comply, and the assets remained protected. In In re Lawrence (11th Cir. 2002), a bankruptcy court took the same approach with the same result. In In re Rensin (Bankr. S.D. Fla. 2019), the court reached a more favorable outcome for the debtor. Courts can impose consequences on the settlor, but the trust assets have remained protected in every contested case involving a properly structured trust.

Why Most Cook Islands Trust Cases End Before Reaching Court

Contested Cook Islands trust matters tend to end in settlement rather than in a Cook Islands courtroom verdict. Plaintiffs’ counsel who locates trust assets after a U.S. judgment looks first at the cost of pursuing Cook Islands litigation, the realistic recovery, and whether settling now for a discount is the better trade.

The pattern we see most often runs as follows. A creditor obtains a U.S. judgment. Post-judgment discovery surfaces the trust. The creditor’s counsel evaluates a Cook Islands filing: a $100,000 bond up front, six-figure Cook Islands counsel fees, a criminal burden of proof, and a deadline that may already have passed. They make a phone call. The opening number is usually well below the judgment, paired with a request for confidentiality and a release.

The Cook Islands trust is built to make a Cook Islands courtroom the worst place a creditor’s attorney could file, not to win once filed. The leverage a settlor holds during settlement is not the certainty of victory abroad but the near-certainty that the creditor’s attorney will not file abroad in the first place. When we counsel a settlor during these conversations, the focus is on letting the creditor’s own math do the work.

The leverage works most strongly in two patterns. Contingency-fee plaintiffs’ counsel will not advance six figures of Cook Islands litigation cost on a recovery they cannot predict. And non-contingency creditors with a large judgment but limited U.S.-side recoverable assets reason that a settlement at a fraction of the judgment today is worth more than a possible recovery years away after Cook Islands proceedings. In both patterns, the creditor’s discount rate on uncertain future recovery is what drives the settlement number down.

Some creditors do press through to a Cook Islands filing. Federal agencies and sovereign litigants with reputational stakes sometimes do, and FTC v. Affordable Media is the well-known example. Even there, the FTC settled with the offshore trustee on terms it found acceptable enough to stop pursuing the assets. Our primary experience over three decades is that the trust performs as leverage even when it is never tested in a Cook Islands court.

What Can You Fund a Cook Islands Trust With?

Cash and securities are the most straightforward assets to transfer into a Cook Islands trust. The trust’s LLC opens an offshore bank or brokerage account, and assets move by wire transfer. The settlor typically continues managing the investment portfolio through the LLC during normal circumstances.

Real estate cannot be moved offshore. Instead, an LLC that owns the property is assigned to the trust. The land remains within U.S. court jurisdiction, which limits the protection. Courts can directly control domestic real property regardless of who owns the LLC that holds title.

LLC and business interests can be transferred by assigning membership interests to the trust. Settlors who own operating businesses or investment entities commonly place the equity beyond the reach of creditors while retaining management control through the LLC structure.

Cryptocurrency presents distinct custody, valuation, and compliance issues. The trust can hold digital assets, but custodial arrangements and reporting obligations differ from traditional financial accounts. Each asset type has specific transfer mechanics, documentation requirements, and potential pitfalls. The funding process is where many structures lose their protective value through errors in titling, account registration, or timing.

Why Choose the Cook Islands Over Other Jurisdictions?

The Cook Islands trust statute was enacted in 1989. U.S. federal courts have ruled on Cook Islands trust cases for more than 25 years, producing the most developed body of asset protection trust case law of any offshore jurisdiction. Other offshore jurisdictions modeled their statutes on Cook Islands law but have less litigation history.

Nevis has a shorter track record and less litigation history. Belize, the Bahamas, and the Cayman Islands each have trust legislation but lack the Cook Islands’ depth of contested case law and dedicated trustee market. The statutory and practical differences between jurisdictions are substantial.

The Cook Islands operates under regulatory oversight that meets international standards. The Financial Supervisory Commission licenses and audits every trustee company. The Cook Islands Financial Intelligence Unit handles anti-money laundering compliance. The jurisdiction signed the OECD automatic exchange agreement, appears on no international blacklist or greylist, and cooperates with tax authorities under the Common Reporting Standard. A Cook Islands trust cannot be characterized as inherently fraudulent when the jurisdiction itself complies with the same international reporting standards as the U.S. and the EU.

Domestic asset protection trusts operate within the U.S. legal system. They remain subject to Full Faith and Credit, federal bankruptcy jurisdiction under § 548(e)(1) with a 10-year lookback, and U.S. courts that can compel domestic trustees. A Cook Islands trust operates entirely outside that system. DAPTs are better than nothing for residents of DAPT-authorizing states who cannot afford offshore planning, but they are not a substitute for a Cook Islands trust.

Common Misconceptions

The most common misconception about Cook Islands trusts is that they can be used to hide assets. They cannot.

Every dollar transferred to the trust must be disclosed on federal tax returns, FBAR filings, and in court proceedings. The protection comes from jurisdictional separation: placing assets under a legal system that does not enforce U.S. civil judgments, not from concealment.

Another misconception is that Cook Islands trusts reduce taxes. The IRS treats the trust as a grantor trust. The settlor reports all trust income on their personal return and pays the same taxes as if the assets were held directly.

Finally, Cook Islands trusts are not illegal. The Cook Islands is a self-governing nation associated with New Zealand, regulated by the Financial Supervisory Commission, and fully compliant with OECD financial transparency standards. Every licensed trustee company is audited, insured, and bonded.

How Is a Cook Islands Trust Managed After Setup?

A Cook Islands trust requires active administration throughout its life. The trustee monitors trust activity, maintains compliance files, and administers the trust under Cook Islands law. The settlor coordinates with a CPA for annual tax filings and with the trustee for any transactions involving trust assets.

The most common administration problems are mundane: delayed filings, informal side agreements between the settlor and the trustee that are never documented, and failure to record the trustee’s decisions properly. These failures gradually weaken the trust’s protection and become apparent only when the structure is tested in litigation. They may also allow creditors to argue that the trustee was acting as the settlor’s agent rather than as an independent fiduciary, which is the argument that led to the contempt findings in Anderson and Lawrence.

Alper Law has structured offshore and domestic asset protection plans since 1991. Schedule a consultation or call (407) 444-0404.