How to Protect Your Bank Account from Creditors

Three factors determine whether a bank account is protected from creditors: the source of the money, the ownership structure of the account, and whether exempt and non-exempt funds are kept separate. No bank sells a product called an exempt account. Protection comes from applying federal and state exemptions correctly, before a garnishment arrives.

A judgment creditor who wins a lawsuit can serve a writ of garnishment on any bank where the debtor holds an account. The bank freezes the funds immediately. The account holder then has a limited window to prove that some or all of the frozen balance is exempt. Missing that deadline can mean losing money that was legally protected.

Speak With a Florida Asset Protection Attorney

Jon Alper and Gideon Alper have designed and implemented asset protection structures for clients since 1991. Consultations are confidential and conducted by phone or Zoom.

Book a Consultation

How to Open a Bank Account That No Creditor Can Touch

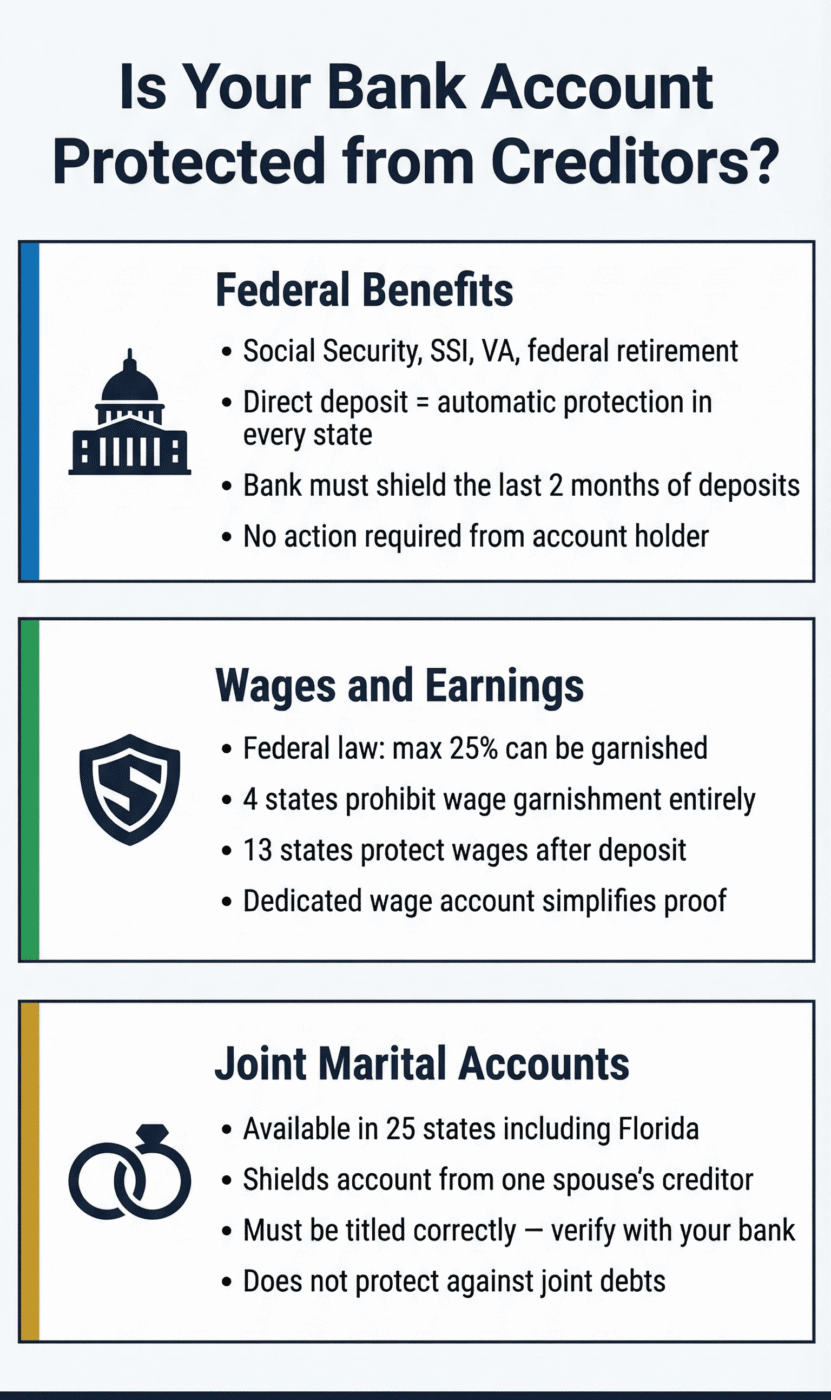

There are five ways to open a bank account that no creditor can touch: (1) Enroll in direct deposit for all federal benefits, (2) keep exempt funds in a dedicated account separate from non-exempt income, (3) use joint marital accounts, (4) maintain a separate account for exempt wages, (5) keep records documenting the source of every deposit.

1. Use Direct Deposit for All Federal Benefits

Social Security, SSI, VA benefits, and federal retirement payments are automatically protected under federal regulation (31 CFR Part 212) when they arrive by direct deposit. This protection applies in every state. The bank must identify these deposits and keep them accessible without any action from the account holder. Paper checks deposited manually do not trigger the automatic protection, which means a simple enrollment change (from paper check to electronic deposit) converts a protection the account holder must prove into one the bank must provide automatically.

2. Keep Exempt Funds in a Dedicated Account

Non-exempt income should never go into the same account as Social Security or other protected deposits. When the only deposits come from exempt sources, every dollar in the account is shielded. Mixing exempt and non-exempt deposits forces the account holder to trace each dollar to its source, a process that fails when records are incomplete. The simplest account structure is one account per exempt income source: a dedicated Social Security account, a dedicated wage account, and a separate operating account for non-exempt funds.

3. Open an Exempt Bank Account

Bank accounts owned jointly by married couples as tenants by entireties are exempt from garnishment by a judgment creditor of either spouse. The accounts are not exempt from the creditors of both spouses, however. Tenants by the entirety ownership of bank accounts is governed by 655.79 of the Florida Statutes.

Not all states offer exempt bank accounts for married couples. Among the 25 states that recognize tenancy by the entirety, some limit it to real estate. Florida is one of a smaller number that extend the protection to personal property including financial accounts. Married couples should confirm whether their state recognizes this form of ownership for bank accounts and whether their bank’s customer agreement supports it.

4. Maintain a Separate Account for Exempt Wages

Many states restrict how much of a debtor’s wages can be garnished. Federal law sets a baseline: creditors cannot take more than 25% of disposable earnings. Texas, Pennsylvania, North Carolina, and South Carolina prohibit wage garnishment entirely for most consumer debts.

Florida’s head of household exemption under Florida Statute 222.11 is among the country’s most protective wage garnishment statutes. A wage earner who provides more than half the financial support for a child or dependent is exempt from garnishment entirely on disposable earnings of $750 per week or less. A dedicated wage account that receives only payroll direct deposits makes tracing straightforward if a garnishment occurs. Florida extends the exemption to deposited wages for six months after the bank receives them.

Other states that prohibit or limit bank account garnishment vary widely in what they protect and when protection expires after deposit. Approximately 13 states explicitly extend wage protection after deposit, while many others treat deposited wages as ordinary cash subject to garnishment.

5. Keep Records of Every Deposit

Monthly statements, benefit award letters, and pay stubs are essential. Every state places the burden of proving an exemption on the account holder, not the bank and not the creditor. A well-documented account is protected; an undocumented one may not be.

What Is an Exempt Bank Account?

An exempt bank account is a bank account containing funds that are legally protected from seizure by a judgment creditor. The exemption attaches to the funds or to the ownership structure of the account—not to the account itself. A single checking account can hold both exempt funds (directly deposited Social Security) and non-exempt funds (rental income), and only the exempt portion is protected. A savings account receives no special protection simply because it is a savings account rather than a checking account—the same exemption rules apply based on the source of deposits.

Every state provides some form of bank account protection, but the scope varies dramatically. Federal law creates a nationwide floor through the automatic protection of directly deposited government benefits. State law adds additional protections that range from minimal (a few hundred dollars in some states) to comprehensive (unlimited wage protection and joint ownership shields in states like Florida).

Three categories of protection are available in most states. Federal law automatically protects government benefit deposits regardless of state. State wage exemptions protect some or all of deposited earnings depending on the jurisdiction. Joint ownership structures protect marital accounts from individual creditors in states that recognize them.

The practical difference between a protected account and an unprotected one usually comes down to separation. Someone whose only income is Social Security direct deposits has a functionally exempt account because every dollar traces to a protected source. Someone who mixes Social Security with business revenue has a partially exempt account that requires documentation to defend, and documentation that may not hold up if records are incomplete. The tracing analysis determines the outcome.

Advanced Notice for Garnishments

A bank account can be garnished prior without notice. A judgment creditor does not need to tell you in advance that it intends to garnish your bank account. If a creditor were required to give a debtor advanced notice of a bank account garnishment, then the debtor would have the opportunity to empty the account in advance of the garnishment.

A creditor must notify you about a bank account garnishment only after first serving the garnishment on the bank. Once the garnishment documents are served on the bank, the bank will freeze the account. The garnishment notice should explain your rights in the garnishment proceeding and the process for claiming any exemptions you have.

Federal Benefit Protections

Federal regulation 31 CFR Part 212 provides the strongest and most uniform bank account protection available in the United States. The regulation applies identically in every state. When a bank receives a garnishment order, it must review the account’s deposit history for the preceding two months. The bank calculates a protected amount equal to the total of directly deposited federal benefits during that period, or the current balance, whichever is lower. That amount stays accessible without any court filing or action from the account holder.

Protected benefits include Social Security retirement and disability payments, SSI, VA benefits, Railroad Retirement, and federal civilian and military retirement. SSI receives the broadest protection—it cannot be garnished even for child support or federal tax debts, which are exceptions that apply to most other federal benefits.

The two-month lookback creates a practical limit. Someone who receives $2,000 per month in Social Security and accumulates a $20,000 balance will find only the most recent $4,000 automatically protected. The remaining $16,000 can be frozen unless the account holder proves through a state court hearing that those older funds also trace to exempt sources. Keeping a Social Security account balance at or below two months of deposits is the simplest way to avoid this problem.

State Wage Exemptions

State wage exemption laws determine whether deposited earnings retain their protected status after they reach a bank account. The differences among states are substantial.

Federal law sets a floor: creditors cannot garnish more than 25% of disposable earnings, or the amount by which weekly earnings exceed 30 times the federal minimum wage, whichever results in a smaller garnishment. Four states go further and prohibit wage garnishment entirely for consumer debts: Texas, Pennsylvania, North Carolina, and South Carolina.

Florida’s head of household exemption under Florida Statute 222.11 is among the most protective in the country. A wage earner who provides more than half the support a child or dependent needs is exempt from garnishment with no dollar cap on wages of $750 per week or less. Florida also explicitly protects deposited wages for six months after the bank receives them, which is critical because many states that restrict wage garnishment do not extend the protection after deposit.

Approximately 13 jurisdictions explicitly extend wage protection after deposit: California, Colorado, Connecticut, Florida, Idaho, Iowa, Minnesota, Montana, Nebraska, North Carolina, Oklahoma, Oregon, and Puerto Rico. In the remaining states, wages deposited into a bank account may lose their exempt character entirely, leaving the funds subject to garnishment as ordinary cash. The state-by-state garnishment laws vary widely enough that a depositor’s protection depends almost entirely on where they live.

Business owners and independent contractors face a threshold question in every state: whether their income qualifies as “earnings” under the applicable exemption statute. Florida courts have denied the exemption to LLC owners who pay themselves through discretionary draws rather than regular payroll. Structuring compensation through a genuine payroll service with fixed salary amounts and employment tax withholding strengthens the exemption claim.

Joint Marital Account Protections

Married couples in states that recognize tenancy by the entirety can shield jointly held bank accounts from the individual creditors of either spouse. The protection exists because both spouses own the account as a single legal unit, and neither spouse’s individual interest can be separated and seized.

Florida provides the broadest version of this protection. Under Florida Statute 655.79, joint accounts between married spouses are presumed to be entirety accounts unless otherwise specified in writing. A 2023 appellate decision in Storey Mountain LLC v. George held that a bank’s customer agreement disclaiming entirety ownership can override the statutory presumption.

Married couples should review the customer agreement before relying on a joint bank account for protection. The Eleventh Circuit’s November 2025 decision in Storey Mountain v. Del Amo reinforced that generic “joint tenants with right of survivorship” language does not override the entirety presumption absent an explicit disclaimer.

Entirety protection does not apply when both spouses owe the debt jointly, when the creditor holds a federal tax lien, or when the claim arises from joint liability. States that do not recognize tenancy by the entirety for bank accounts offer no comparable joint ownership protection.

Digital Wallets, Online Banks, and Fintech Platforms

Cash App, Venmo, Chime, PayPal, and similar platforms are subject to garnishment under the same rules as traditional bank accounts. A creditor who locates the account can serve a garnishment order on the institution. No financial institution can override a valid court order, and no fintech platform is exempt from garnishment simply because it is not a traditional bank.

The same federal and state exemptions apply regardless of where the account is held. Social Security deposited into a Chime account receives the same automatic protection under 31 CFR Part 212 as Social Security deposited at a traditional bank. Florida head of household wages deposited into Cash App retain their six-month exempt status, identical to wages at any traditional bank.

Fintech platforms that have marketed themselves as “garnish free” or exempt from levies have no legal basis for those claims. Digital wallet garnishment follows the same procedural rules as garnishment of any traditional bank account, and the platform’s structure as a non-bank intermediary does not change the outcome.

What Does Not Protect a Bank Account

Several commonly suggested strategies are ineffective or illegal.

Transferring funds to a family member’s account after learning of a lawsuit or judgment is a fraudulent transfer. Every state has a version of the Uniform Voidable Transactions Act (or its predecessor, the Uniform Fraudulent Transfer Act) that allows creditors to reverse these transfers.

Opening a bank account in another state does not help if the creditor can locate it. After obtaining a judgment, creditors use court-ordered discovery tools to identify financial accounts anywhere in the country. Lying under oath about account locations is contempt of court. Opening a new account after a bank levy does not reset the process either, though exempt funds deposited into the new account retain their protected status.

In-trust-for and pay-on-death designations do not protect funds from the depositor’s creditors during the depositor’s lifetime. These designations affect who receives the money at death, not whether creditors can reach it before death. An ITF account structured as a genuine irrevocable gift is an exception, but the account holder must have truly surrendered control—which most ITF accounts do not accomplish.

Keeping large amounts of cash outside the banking system avoids garnishment but creates risks including theft, loss, and inability to prove the source of funds if an exemption claim is later needed.

When Domestic Exemptions Are Not Enough

Federal and state bank account exemptions protect income that individuals need for basic living expenses. They are not designed to shield substantial liquid wealth. Someone with $500,000 in non-exempt cash will not find domestic exemptions sufficient regardless of which state they live in.

For individuals with significant liquid assets and meaningful creditor exposure, offshore accounts held through foreign legal entities and irrevocable trusts established in asset protection jurisdictions create legal barriers that domestic judgment creditors cannot easily overcome. A Cook Islands trust paired with an offshore LLC is the most widely used structure for this purpose. These structures involve costs, compliance obligations, and tradeoffs in access and control that should be evaluated before implementation.

The threshold question is whether available domestic exemptions cover the amount at risk. For someone whose bank account contains only Social Security and exempt wages, the framework described above provides all the protection needed. For someone with substantial non-exempt liquid assets, it will not.